Paper & Packaging

North American paper and pulp producers face a rapidly changing landscape. Paper used for communication purposes is in decline due to electronic media. Packaging grades and tissue / hygiene products offer better demand characteristics. Paper packaging is also benefiting from sustainability advantages.

However, sectors with better demand are attracting additional competition from new machines and publication papers machine conversions.

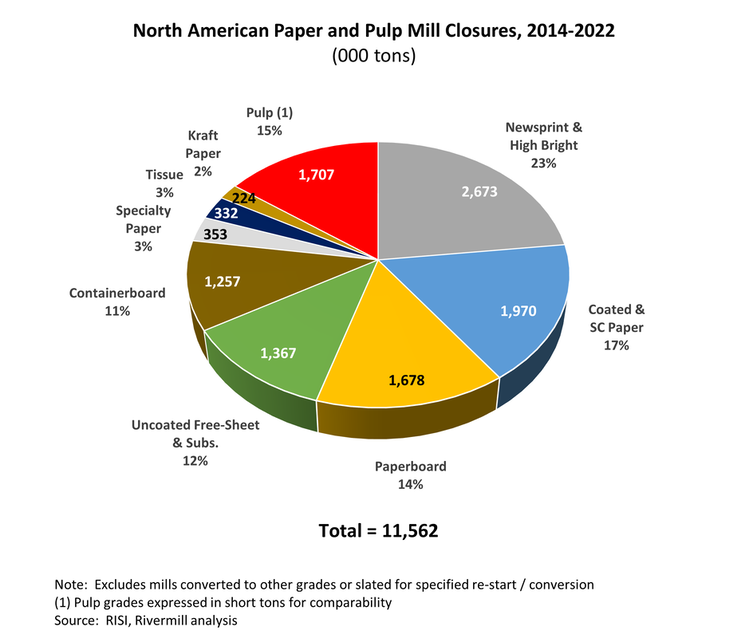

The result has been the closure of at least 59 North American mills with 11.6 million tons of capacity since 2014.

However, sectors with better demand are attracting additional competition from new machines and publication papers machine conversions.

The result has been the closure of at least 59 North American mills with 11.6 million tons of capacity since 2014.

Click chart for detail on mill closures since 2014

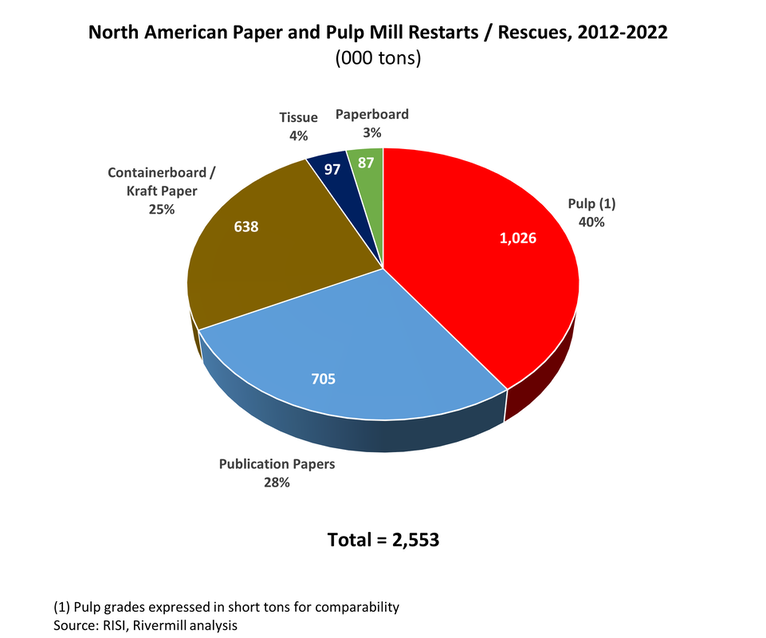

Some mills have sustained or restarted operations by attracting new investors based on their presence in attractive markets and operational restructuring initiatives.

Some mills have sustained or restarted operations by attracting new investors based on their presence in attractive markets and operational restructuring initiatives.

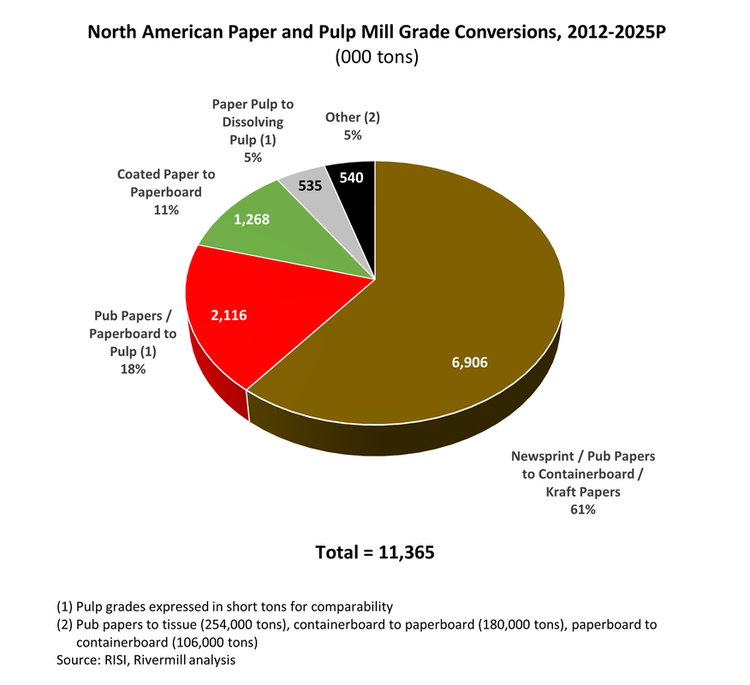

More capacity has avoided shutdown by converting to new products.

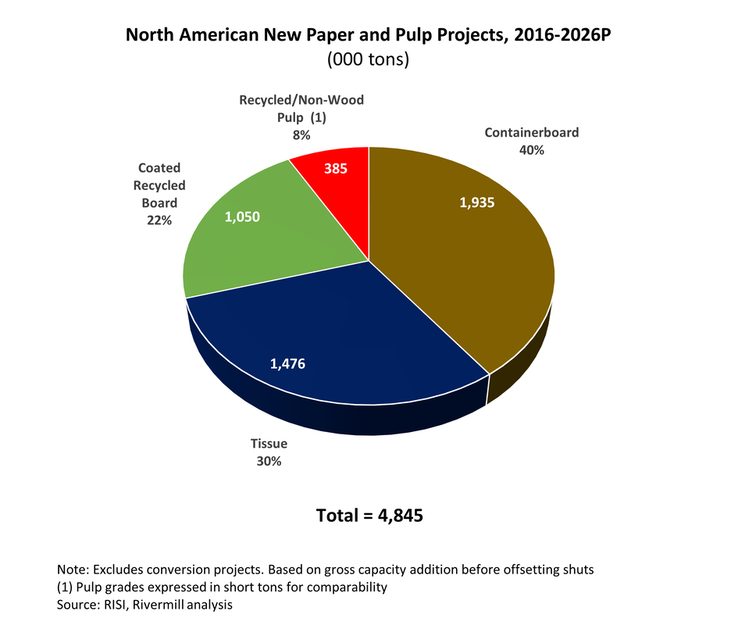

In addition to conversions, growth grades including containerboard, tissue, paperboard and pulp are attracting new capacity investments.

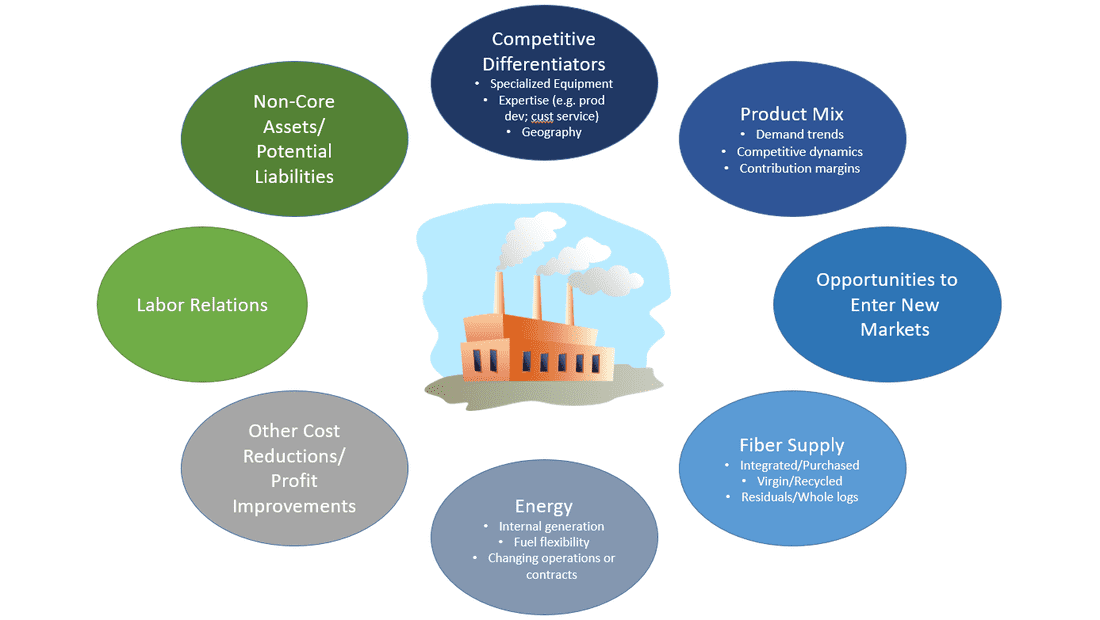

This competitive environment means that every mill needs to focus on the capabilities and assets that will continue to make it viable. We have worked closely with both profitable and struggling mills across the range of grades including newsprint, printing and publication papers, packaging, specialties and tissue.

To attract new investment, we focus on framing a compelling selling proposition and the key competitive and operational dynamics for the business.

To attract new investment, we focus on framing a compelling selling proposition and the key competitive and operational dynamics for the business.

We have a strong understanding of the strategic competitors and financial sponsors interested in investing in the sector. Click here for detail on recent mill-related transactions.

We are proud to have been involved in many successful sales of profitable mills and turnaround / restart projects at predecessor firms.

We also apply our sector expertise to projects in packaging / converting, distribution, and equipment / consumables vendors to the sector. We leverage our understanding of:

- North American and global supply / demand dynamics

- Knowledge of key competitors and interested private equity investors

- Interest in forward integration in sectors such as corrugated packaging, folding cartons and tissue